“There’s this wild disconnect between what people are experiencing and what economists are experiencing,” says Nikki Cimino, a recruiter in Denver.

Hey, somebody’s gotta pay for the highest corporate profits in 70 years.

Important to note:

Companies aren’t just raising prices enough to cover costs, they’re padding their margins on top.

Just saying that their profit is higher means nothing because of inflation. Inflation will mean that their profits are more often than not the highest they have ever been every year. But the highest margins? That shows they are price gouging.

If you want to know how bad we’re being fucked, search for the PPI, the producer price index. CPI, the one we always hear about, is the measure of inflation to us, the consumer. The PPI is the measure of inflation to producers, what they pay for goods and services to produce the goods and services we buy.

The PPI has been back to “normal” for a while now. Pretty much as soon as the post COVID logistics issues were mostly ironed out. The difference between PPI and CPI changes is almost all profit.

We don’t get daily articles on the PPI though, I wonder why.

Tell people about PPI whenever you can, online or off, the more people know, the better. It’s easy enough to say inflation is just down to greed but being able to back it up by comparing two simple charts will help people really understand.

I couldn’t find a comparable historical CPI chart on the BLS website, just a 12 month average and historical data by region. Are you able to find something to compare that chart to? It’s kind of difficult to grasp intuitively (without a comparison, that is).

I edited the links to try to get more apples to apples. For the PPI just deselect the blue line and compare red lines between the two. Those should give 12 month change numbers for all goods and services unless I screwed it up.

Edit: I edited the links again, I accidentally used final demand instead of intermediate demand for PPI. No need to deselect anything now. I linked the chart for processed goods, other categories are available in the drop-down list.

Thank you! And thank you for finding and linking all that, it is very informative!

Exactly that. On average the economy is doing fine but it’s skewed very heavily towards the top and nothing much for the 90%. The median income is actually decreasing.

Removed by mod

I would LOVE to see a source on this, but I have a feeling I already know where it is coming from.

Would you prefer the Economic Policy Institute, Politico, or CNBC?

None of this matters when low income people have been getting screwed for 30 years. 3 years of growth means almost nothing when you put it in proper context. It’s just a way for the upper class to gaslight people.

There are people out there still getting paid $9 an hour which wasn’t liveable 15 years ago when that was my wage. If this trend continues, calling it wage slavery won’t be hyperbole anymore.

Plus none of these articles talk about the middle 80% who have not seen their pay keep up with inflation over the last 5 years, or the fact that the price of many goods has exceeded inflation on top of that. Not to mention the housing crisis.

It’s not hard to figure out why people think the economy sucks.

There are people out there still getting paid $9 an hour

There are now fewer people out there still getting paid $9 an hour. Why are you against progress?

“Things are better but still not perfect therefore this is meaningless” is a terrible take.

Yes, bottom 10% are doing better and the top 10%. That means the middle is getting hollowed out and the whole thing turns into a very divided society. That’s not a good thing.

It’s not a good thing, but it’s better than the blatant “rich get richer, everyone else gets fucked” economy we’ve had for the past few decades.

And doesn’t it make sense that we improve the situation of the poorest first?

blatant “rich get richer, everyone else gets fucked”

and now you have a rich get richer, almost everyone else gets fucked economy. Yay, progress.

Looking at history, it feels more like an attempt to make sure the poorest don’t fall into the “nothing left to lose” category that can cause so much trouble.

Oh no, what a…terrible…thing…?

and now you have a rich get richer, almost everyone else gets fucked economy. Yay, progress.

Yes. Things were more bad, and now they are less bad. Vote in more Democrats, and things will continue to get less bad. Eventually, things will be good. That’s how progress works.

There’s a term for this, HENRY. High Earner, Not Rich Yet. The lie is the “Yet”. Millennials and Gen Xers have been struggling to reach the middle class that is kept perpetually out of reach. They have given up on the idea of financial solvency and are going into debt to indulge in luxuries like having children, going on vacations, and living somewhere that isn’t a complete shithole. Saving for retirement is as realistic as training to live on Mars, so why bother? Keep digging a financial hole and then lie down and die in it.

Gen X here and I can’t afford to contribute to my retirement. Even had to withdraw some during unemployment. I’m either working until I die or hoping assisted suicide becomes legal in 20 years.

Yep. Same. I do pretty good for myself and I’m more fortunate than most, but I had to borrow money from my dad recently for a series of expenses I couldn’t absorb in real time. I got the “you don’t know how to budget” sermon. It felt as fun as you’d expect

I said fuck it and gave him a list of earnings and expenses (I’m pretty frugal) and he was like, “oh…”

assisted suicide

Is that when you die but take a billionaire with you?

X here too, 53yo, cannot contribute to retirement. At 67 I will have to sell my house because I’ll not be able to afford taxes, insurances, power, repair, etc

Assisted suicide vs… illegal suicide? What’s the difference?

Illegal doesn’t pay out insurance claims. Not that I can afford life insurance….

I might be “rich” when my parents die, depending on how much elder care they need.

I’m actually kind of looking forward to the day I look my kids in the eye and say “I’m going out to look for firewood” and just walk out into the snow and die.

But there won’t be any snow anymore so I’ll just wander off into a slightly chilly night.

slightly chilly night.

You’re a glass half full kind of person, aren’t you?

You should watch the movie The Road if you haven’t already.

What most people don’t realize is that once you have excess income, you have options. What you do with the excess is what matters. If you don’t save and invest it, you’ll be living paycheck to paycheck for the rest of your life.

A lot of folks think being rich means just spending money on whatever you want. That’s not really the case. If you spend the excess on fancy cars or luxury items that make others think you’re rich, the irony is you’ll be working for a long time and never actually become financially independent.

Edit: well, if I’ve learned anything from this comment, it’s that everyone on Lemmy identifies as a HENRY with bad spending habits no matter how much money they make. Or, at least a temporarily embarrassed one.

Except that’s not at all what OP said or was implying. Nice way of pushing the blame on the people affected rather than the broken system we live in.

Both can be true. There are many people who barely (or don’t) make enough to survive. There are also many people who spend money frivolously and then complain that they’re broke because of the economy.

Most people are struggling with the basics, not disputing that. But, then I wouldn’t consider those people HENRYs.

When I look around, I also see a lot of people with high income making boneheaded moves like buying expensive vehicles, renting luxury apartments, etc. For some people the problem isn’t the system, it’s their own lack of self-control or planning. If you’re making $200,000 and still feel broke. Maybe that $1,500/month car payment was a mistake. Maybe you shouldn’t have used the raise to move into a luxury apartment building.

When I was starting my career all my coworkers lived in $2200/month luxury buildings. I knew we all made roughly the same amount of money, so was shocked that they would pay this much for rent. Meanwhile, I sought out roommates and paid $650. With the money I saved, I paid off my student loan debt aggressively. Now all these people are struggling to get to the next step in life. Yeah, I could’ve seen that coming 10 years ago for you.

I see the same thing with cars. Everyone wants to own some luxury SUV. And, they make fun of me for driving a Prius. I won’t be surprised in another 10 years when they’re still struggling.

This isn’t an attack on people who don’t have the money. This is an attack on people who do and can’t plan well, but then act surprised when they’re broke still.

I gotta back your position here, especially because I think you’re being downvoted unfairly. There is a lot of unfairness in this economy for sure but on this thread that started with HENRY and literally “They have given up on the idea of financial solvency and are going into debt to indulge in luxuries” your comments are totally in line and fair.

Want to add too, that even the first subject in the article ‘Making the most I’ve ever made’ isn’t the best example of a tough economy. She went through a divorce and then bought a house in one of the most competitive housing markets in the US. The high interest rates certainly make that tougher but that’d be hard to afford even before without it.

I don’t make 200k, but together with my wife, we make a little under that. We both have cars, and both are paid off. I still have the first car I ever brought, which is a Nissan Sentra 2006 basic model. So, 17 years on the same car and hers is a 2015 Toyota. We do have 2 kids and brought a house in 2015. The last 4 years have been almost impossible to make ends meet, and all we try to do is survive with the very occasional do something for the kids. I have tons of housework I can’t do but also can’t pay for either. Because of this, we also can’t move until it’s taken care of, so we’re kind of stuck here as well. We have no money to save or invest. Did we make some bad decisions? Sure, probably shouldn’t have had kids for starters. They cost a fortune. But my point is we aren’t doing anything crazy here, it’s just that more and more things are taking our money and prices also went up. It sucks because all I want to do is live and get by, I don’t really have any grandiose dreams of doing crazy things or buying tons of stuff. I just want to get by as my parents did, which seems impossible today.

How much did you pay for your house? Assuming you live in a HCOL area? Making almost 200k you shouldn’t be struggling at all, unless you’re living in some crazy high cost of living area.

I live in North NJ. From my understanding, it’s about as bad as it gets. House was 330k 10 years ago. We also have crazy property taxes, so that alone is 13k a year. I also live in a very rural area which was the only option for the area if we wanted some space and also keep house prices semi cheap.

How damn costly is everything else there, that’s crazy high for property taxes though.

Even if you do nothing, if you don’t get into debt, you will have millions in equity in the house when it’s paid off.

You’ve basically invested into real estate so you’re saving money even if it doesn’t go into your savings account.

We purchased the house for around 300k, and even with the market today, it’s about 500k. Sure, it could go for higher whenever we do sell, but it’s not an investment. With our current loan we will have paid over 500k over 30 years, so I really am not expecting to make out from this. The only way this makes me money is when I retire (which is close to payoff anyway) and move someplace way cheaper than we’re we live now.

You’re going to pay it off in what, like 25 years? Yeah, it will be worth over a million by then.

My dad bought his house for $600,000 in 2008 peak, and it is now worth maybe 2 million. It hasn’t even been twenty years and it’s more than tripled, despite being underwater on the mortgage in 2009 (owed more than market value)

Every time ive tried investing, i had to take it out after a few months to pay for something thats popped up in life after other things have raided my savings.

Investing is for people with a lot of excess cash.

Precisely, which is why I don’t think my comment is directed at you. If you’re always trying to get ahead of the latest unexpected big expense, you’re not a “HENRY.”

That’s what living pay check to pay check is though…

Not necessarily. It’s what living paycheck to paycheck is if you’re poor. If you make a lot of money but spend a lot of money on unnecessary things you can also be paycheck to paycheck.

If you don’t save and invest it, you’ll be living paycheck to paycheck for the rest of your life.

I don’t think you really know what “living paycheck to paycheck” actually means if you think it, in any way, involves investing.

I think his point is people are only living paycheck to paycheck out of choice when they could save and invest if they tightened their belts.

Not saying I agree, just explaining his perspective.

There are peple who are genuinly struggling.

Then there are those who choose to spend 10-20K on vacations every year and ‘feel’ they are struggling.

And these latter people will forever tell you how they are living ‘paycheck to paycheck’ and talk your ear off about how theri struggles are more genuine and ‘real’ than people who are actually poor.

Maybe if they ate less avocado toast right!

You can have very high income and still live paycheck to paycheck if you spend every paycheck

“living paycheck to paycheck” generally means that all money is spent on living expenses and there is very little, if anything, left over. If you have any appreciable discretionary income, you are not living paycheck to paycheck.

Tell that to the people who make 150K and spend 200K a year.

Hint: they dont’ give a shit what you say.

I’m not concerned about what those people say; they are doing just fine. I’m concerned about the people who are actually living paycheck to paycheck.

This is really stupid.

You’re basically telling people “just be rich” like it’s that simple.

People living paycheck-to-paycheck are not able to invest money because they don’t have excess income, they get to decide if they want to pay for rent or want to pay for food. Combine that with astonishing inflation rates and salary raises that don’t match cost of living increases or simply layoffs, and we have one fucked up situation.

This is a systemic problem. Billionaires shouldn’t exist. Billionaires are a societal problem.

edit: Oh, I see your comment isn’t directed at people living paycheck-to-paycheck, that’s a bit more reasonable then but I still think you’re missing the mark. It’s not as simple as “just increase your income” like you seem to be thinking it is.

because it is that simple.

be rich or forever be poor.

this is the system we have setup and the system that we worship.

I try to save whatever extra I have, because everyone says I need to have six months of expenses saved.

The problem is that before I can save up enough to cover that there’s some huge expense that I need to cover that empties it out and puts me even more into debt.

If I could manage to save up a year of expenses, I could probably start my own consulting agency and start making a lot of money, but I just can’t get there.

The problem is that for many folks the amount they are making isn’t enough for them to live a very reasonable life AND they have nothing to invest in the first place. Suppose a household in a given area needs $100,000 to afford a VERY modest house in that area, health insurance, savings, healthy food etc. Now suppose the house has one disabled breadwinner and one fellow working for $40,000.

Because of this they live in shit town in a tiny apartment a building full of drug addicts in a not so great part of the state wherein the average life expectancy is about 10 years less than one of the good parts of the country.

The first 40k of “excess” would be spent on having a decent life, working a sane number of hours, moving into an actual home. For fully half the country the idea of having excess is laughable. It’s a crass joke.

Most areas don’t need $100,000 a year to afford a “very modest house”, you could get a nice mobile home and afford to pay off the loan in just a couple years.

the areas where most people live, however, do.

nobody wants to live in trailer park in Mobile, AL.

Why not?

Lets define “most”. Herein I define most as the area immediately surrounding the majority of people. 70% of people live in urban areas not out in bum fuck.

I live in a small city of 50,000 in Washington. A house around here starts at about 400k. I would have to pay about 3100 per month including taxes and insurance. I would take home about 6500 per month after taxes if I made 100k. At current interest rates I would need to spend 3100 per month to service such a loan.or about 47% of my take home pay. It is difficult to see how I could afford a home with a household not individual of less than 100,000.

Adjacent to me is a much bigger city with about 20x the jobs and opportunities. I would need more like 900k to buy into there. Realistically to afford a home there we are talking about my household making more than 200k. Why so much? Because housing has got very expensive and interest is very high.

A ton of urban areas have much options cheaper than the west coast though, mobile homes, townhouses, duplexes, etc. $400,000 is much more than a very modest house. For example I would consider a shotgun house very modest, and short of very high income areas they’re usually much less than $400,000

Cheaper places are cheaper for a reason. Worse health care. Worse education for your kids. Worse life expectancy. Worse Opportunity. For instance St Louis has a median home price of 207k but they also have 10x the murder rate of Seattle a worse jobs outlook. You’ll make less money etc.

Who in their right mind would want to live in a red state?

Cheaper places are cheaper for a reason.

Yes, and I agree I prefer higher density, but ultimately some people living in less desirable areas is more reasonable than trying to build ever taller skyscrapers in city centers- in a country with massive amounts of empty land.

Worse health care.

It depends, there are plenty of cheaper cities with very good healthcare, I grew up in Louisville, KY, spent a lot of time in LA, CA, and now live in Prague, CZ. Louisville has had the cheapest rent/purchase price and had by far the best quality healthcare(at least that I and my family received) out of anywhere I’ve lived.

Worse education for your kids.

This is valid in some cases, and there are plenty of valid reasons to desire living somewhere else more, that doesn’t mean there aren’t costs to that. Furthermore, there are plenty of expensive places with terrible school systems, plenty of cheap places with passable school systems, but more importantly traditional schools systems in general suck. Kids now days have access to the internet, that combined with parents who encourage curiosity and creativity will be much more important to them learning than the school system they go to.

For instance St Louis has a median home price of 207k but they also have 10x the murder rate of Seattle a worse jobs outlook.

That is cherrypicking, compare Chicago to Fargo, ND. Or a less distant example, Seattle to Spokane.

You’ll make less money etc.

Assuming you don’t work remotely, but you’ll also spend less.

Who in their right mind would want to live in a red state?

Not about being red or blue, its about not being a HCOL megalopolis. You can also move to Maine.

what the heck’s a rimjob?

I had dinner with my mom last night. She told me she made $2.20/hr as a waitress in 1972. Not including tips.

That’s the equivalent of over $16/hr now.

The boomers have no idea how lucky they were. And they fucking wasted it.

They weren’t lucky. They voted for people that removed all the guardrails that enabled their success.

I agree. I still think they were lucky insofar as they were born in the right place at the right time to benefit massively over future generations.

They had too. They couldn’t get rich if they had to pay workers what they were paid when they were starting out.

Waiters today make $2.13 an hour in my state.

As much as you complain about the boomers, the current generation(s) are the ones you need to pay attention when it comes to who’s caused the house shortage because of unchecked capitalism. There’s more than enough houses that should house everyone for cheap.

You cannot blame boomers for the smouldering wreck that Airbnb left behind. That was the work of a millennial. Take some responsibility for yourselves and your own actions that have attributed to the current state of society that you live in.

My guy, air bnb didn’t cause the shortage or even significantly make it worse. It’s the mega corps that literally own hundreds of thousands of homes across the US and just rent them out. I’m not even upset at boomers who own 3 or 4 rental properties and I work with a lot of them. It’s always mega corps fucking it up for the rest of us.

Megacorps aren’t in general ‘boomers’

mega corps span all the recent generations.

And fuck off with this ‘my guy’ bullshit you sexist, condescending git.

Housing was wildly expensive and rising incredibly fast before Airbnb was invented (company started in 2008, which you might recognize as an important year for the real estate market). After 2008, tons of investors came in to buy up the depressed value properties to either flip or rent out or just hold onto until the value returned. People buying houses with cash isn’t something Airbnb caused. Corporations buying up houses to rent isn’t something Airbnb caused. Foreign investors buying up houses to get their money out of their country isn’t something Airbnb caused.

Airbnb invented a way to make money off of housing by taking houses away from people. Entire blocks will be bought by a company just to use as an Airbnb hence why a lot of stipulations have been recently coming in to prevent a ‘housing shortage’ while there’s enough housing.

So yes, Airbnb did a lot of damage there when it comes to ‘who can we pin ideas on’ blame which we love to do so much to boomers.

LOL you really believe that “a millenial” created AirBNB and not some conglomerate of venture capitalists funneling billions at a team made up of people of all ages?

No shit. So you agree It’s not just boomers. Now go get mad at the OP for spawning this stupid nonsense argument in the first place. Go on and grow that attention span.

Seems you think that I am responsible for your anger. Weird.

Seems you think everyone is responsible for you aside from you

Ow, burn!

Wtf even does “the current generations” mean? Whenever people say “the newer generation” or “the young generation” or something they just sound so fucking incompetent.

And worse: the home buying age isn’t 19, it’s more like 30 - 40.

Being over 40 doesn’t make you a boomer.

As is blaming boomers when the world is not run by just that one generation. The most successful billionaires today are made up from genx and millennials.

So making it a generation war just when it’s pointed at boomers is just stupid and incompetent for an argument.

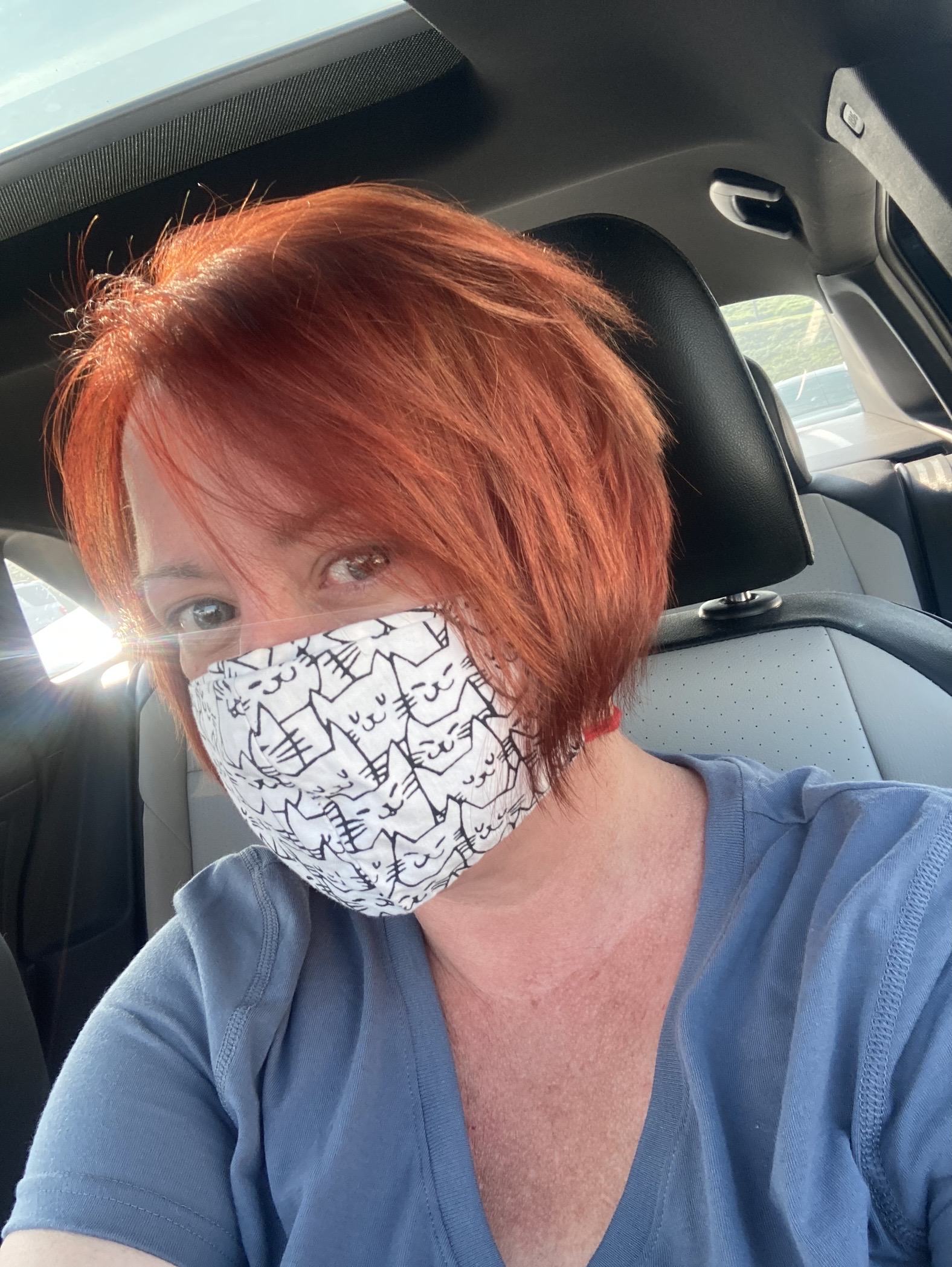

Nikki Cimino, a 40-year-old recruiter living in Denver, said she finally saved up enough to buy a condo last year, but missed out on the ultra-low interest rates that had made homeownership more affordable in the early days of the pandemic. Her 5.25% interest rate pushed her monthly payments to $1,650. After a divorce in 2020, she’s shouldering $4,000 in credit card debt.

It’s the credit card debt…

Instead of paying that off since 2020, she saved a down payment and bought an expensive condo. She’s wasting a shit ton of money on interest because credit cards are all like 20-30%

Credit cards are predatory, if you ever carry a balance to the next month, that needs to be your highest priority.

Do a transfer to get 0% each year if you have to when recovering from emergencies. But paying credit interest for years is insane.

Bingo. I never, ever let credit card debt carry over. I’d genuinely rather miss a house payment.

For Denise and Paul Nierzwicki, credit cards are the only way to make ends meet. The couple, ages 69 and 72, respectively, have about $20,000 in debt spread across multiple cards, all with interest rates above 20%.

The trouble started during the pandemic, when Denise lost her job and a business deal for a bar that they owned in their hometown of Lexington, Kentucky, went bad.

They applied for Social Security, which helped, and Denise now works 50 hours a week at a restaurant. Still, they’re barely scraping together the minimum payments for their credit card debt.

Jesus. I don’t see how this gets un-fucked without a massive wave of defaults. And that’ll just lead to a different kind of fucked.

Her mortgage is $1650/mo, which is incredibly reasonable in Denver. I think this specific person’s problems have more to do with her recent divorce. She was used to splitting costs, and probably spent quite a bit on the divorce itself

She’s paying $1650 for a house? You’d pay more for a house in a neighborhood where every night is the purge here.

That’s supply and demand, for you.

…that’s more than I’d make with minimum wage in my state, which I don’t think is that far behind colorado. Yikes.

ETA: ok nvm I did math and if you make a little over $10/hr 40 hrs a week, your entire paycheck would go just toward that.

You’re still off unfortunately.

Full time at $10/hr is $1600/month before income tax. For simplicity, we’ll say federal+state tax is 15% so now we’re at $1360. Social security is 6.2% so take away another $100.

Then, of course, this is the United States where most people have to rely on their employees for “affordable” health insurance - and often still have money taken out of their check for it.

So now we’re at $1000-1260 monthly take home pay for a full time job at $10/hr

“affordable” health insurance

At that income, you would qualify for Medicaid.

Also I don’t think you pay income tax when your income is that low.

deleted by creator

The standard deduction is $13850 so there’s no way you’re paying 15% tax on an income of $20,000

You’re paying about a little over $600 federal plus whatever state tax and usually state tax is less than federal, but depends on the state. In some states you don’t pay state income taxes.

So best case scenario you pay a little over 3% federal and no state.

At that salary you’d also get EIC and likely pay no taxes at all.

Someone making minimum wage is unfortunately not likely to be getting a mortgage.

I pay more than $2k for a 1-bed apartment in Seattle. Would love that rate for sure.

As someone with mortage of 520€/month there’s nothing reasonable in what she’s paying. I don’t care if it comes with 6 bedrooms, a maid, cook, gardener and a chauffeur - I’m not paying that. I’m more than fine in my tiny granny cottage on the outskirts of a middle sized city.

You couldn’t rent a shack that had a floor made of perpetual dirty needles for $520/month near me.

The floor is rising! But, the floor is lava.

But the lava is tax deductable

But you need an attorney to claim the deduction

Like Dubya said, you should get 2 or 3 more jobs so you can put more food on your family.

“You work three jobs? Uniquely American, isn’t it. That is fantastic that you’re doing that. Get any sleep?” - President George Bush to a divorced mother of three. Omaha, Nebraska Feb. 4th 2005

Proof you can’t die of cringe

That requires self awareness

Well he is a war criminal so I don’t think he feels shame like a normal person would.

How else is she going to put food on her family?

Aahahaha Bush’s malapropisms, a gift that never stops giving

Most of them were said by Dan Quayle.

I’m in this article and don’t like it.

A higher quality of living is being gatekept by the wealthy.

Consider the possibility that, first and given the political importance they have in the present day, the official numbers that the Economists are using are less than honest.

Also, I know that some countries don’t include Housing Inflation - which is huge* - in their Official Inflation. Is that also the case in the US?

Last but not least, there is the whole difference between what is usually reported to us by Politicians, Economists and the Press, which is either country totals (which grow up merelly by the population growing) or the mean average (i.e. adding all values and dividing by the total number of points) which suffers from the “if a man has 10 chickens and 9 others have none, each has in average 1 chicken even though most have none” problem, and the mode (the value around which most cases are found) which is far more representative of most people’s experiences: if for example the wealth increases from higher productivity are going entirelly to a few people who just get ever more filthy rich whilst the many have either stagnated or, worse, are getting a bit poorer due to inflation eating up the true value of their pay, the grand total will be growing, as will the average (if the population numbers are steady) but the mode will have stagnated or even be falling, matching the experience of most people - people get to hear about country GDP growing and even GPD-per-capita growing all the while the vast majority see not growth at all, maybe even a falling of their purchasing power (the latter for sure for any who don’t already own their house).

Been arguing for years that the Mode is far more representative of the common person’s experience than Mean or Median. Most ppl don’t remember that Mode even exists.

All three should be reported, along with raw data. Maybe it’s available somewhere, I haven’t looked.

I’ve never understood why median is a useful metric.

Apparently inflation went down bigly in the 1980s when they decided to stop counting the cost of housing. NPR last week had a report about people advocating to put that back in so that we can have a better idea of what is going on.

Well, the official Inflation is used in the calculation of the official GDP were it acts as a deflator (i.e. the more the inflation the less the GDP) to correct the Nominal GDP (which is in present day currency terms) to make the Real GDP (which is supposedly free of Inflation and hence comparable between years) aka the Official GDP.

If the official Inflation understates the real Inflation, what happens is that the increase is the Nominal GDP that comes merelly from inflation rather than from any actual growth in wealth, is not fully offset when the Real/Official GDP is calculated, so the resulting “real” GDP number is bigger than reality and proud government politicians can come out, compare it to last years’s GDP (which it should’ve been comparable with, if both were done properly) and claim that it was their steering of the Economy that made such a difference to last year’s GDP, i.e such high GDP Growth.

Hence the is massive political pressure to understate Inflation, i.e. to lie, so that ultimatelly larger GDP Growth figures can be posted and boasted about.

Money is for corporate people, not normal people! Silly goose

Honest work: You make just enough to live on until its not enough and then you’re homeless

Scams and grifting: You make possibly lots of money then maybe get sent to jail which is where the courts are gearing up to send homeless people anyway.

Every year the value of our money goes down because the government keeps printing more of it like its a cocaine addiction (This is on top of prices going up for other reasons as well).

Unless you’re getting huge raises every year you’re never going to get ahead, and if you’re getting nothing, you’re actually losing money.

It’s way worse than that.

I suggest you go read the paper entitled “Money

makingcreation in the modern economy” from the Bank Of England, but I’ll summarize it here:- In the modern economy money is almost entirelly numbers in computers and most of it is created by banks when they extend loans (they literally create that money right then and there as two entries in two ledgers, one a credit on the account of the lendee an another a debit on a special account of the bank saying that they are missing that much money).

The “good” old days when all the money was created by governments has been gone since the 90s and the advent of digital account keeping and digital money transfers. A banking license is de facto a license to print money, though within certain conditions, with central banks somewhat limiting that money creation by imposing reserve ratios on banks (i.e. money that they do have to put aside against those outstanding loans) which can be as little as 2% of the outstanding amount.

Edit: the title of the paper was slightly wrong. Also, here is a link to it.

90s and the advent of digital account keeping and digital money transfers

Digital account keeping has been a thing since the 1950’s. And doing it on a computer didn’t change that all banks lent out more than they had. It’s the premise of the movie It’s a Wonderful Life. Bank runs were a thing for as long as banks have existed.

There’s a lot more to it than just that (such as, how do banks settle interbank transfers or even things like how the end of the gold standard paved the way for it) but I didn’t want to complicate the explanation with too much details, though the main difference is the widespread use of digital transfers, especially by consumers which actually dates back a bit further than the 90s but definitelly not all the way to the 50s.

If you really want to know it in depth, I recommend you read the paper I pointed which is here. (By the way, I got the name slightly wrong: it’s “Money creation in the modern economy”)

Digital transfers are not necessary for banks to loan money. As your link says, it’s the loan, which gives money to a business or consumer that the bank doesn’t physically have, that creates money.

Electronic fund transfers and ATM’s started in the 1960’s. Nasdaq the first completely computerized exchange (no people involved) started in 1971.

Digital transfers are now the dominat way for money to be exchanged in trades, replacing mainly cash, i.e. the coins and currency that can only be made by the Mint.

The less people use cash to pay, the less the cash withdrawls from the banks, the less the banks need to procure cash - in a world world were payments are almost all done via payment orders, typically digital, the banks only need to procure cash for periodic settlement of the differences in payments between them: for example, if person 1 does an electronic transfer of $1000 from their account in bank A to person 2’s account in bank B and person 3 does an electronic transfer of $900 from his account in bank B to person 4’s account in bank A, all that bank A has to procure to settle the difference is $100 and bank B nothing at all, even though $1900 changed hands between various otherwise unrelated parties. If they were cash transfers, bank A would have to get $1000 in notes and coins from the mint (to give to person 1) and bank B would have to get $900 (to give to person 3). Now imagine this times hundreds of thousands fold of transactions a day and you can see how much money can change hands without the banks having to get the actual coins and notes (or treasuries and so on: the stuff they can’t produce) that ultimatelly would come from the government.

This is also possible with cheques, but it was the widespread use of electronic transfers, namelly electronic payment methods, that really reduced the need for banks to procure actual money tokens that they can’t legally make themselves, such as cash.

It wasn’t the invention of electronic transfers that made this happen (as I said, cheques also enable a similar thing), it was its widespread use - replacing most cash transactions out there - that made this mechanism become dominant over the traditional one were banks needed to get cash in as deposits so that they could give cash out as withdrawals that then were used by people and businesses for payments and came back on the other side as deposits.

Without such a high need to provide cash to their customers, banks can have a much higher percentage of IOUs (in the form of mere numbers in computers) to cash than before only requiring cash (and ither such forms of money such a treasury certificates) for the periodic settlement of the pending differences between banks of inflows minus outflows, ad per my example above.

namelly electronic payment methods

People don’t venmo at grocery store checkout. It’s all credit cards. The credit card craze started in the 60’s which unsurprisingly coincided with banks switching to eft’s.

Credit cards are electronic payments, hence why they had magstrips and later smartchips. Also how long ago did they replace most cash transactions depends on the country - in plenty of even Western nations card payments were pretty rare even it the 90s.

Thwt said your point that fhe transation to said “modern” economy has been going on for longer than merely “since the 90s” does make sense.

Unless you’re getting huge raises every year you’re never going to get ahead, and if you’re getting nothing, you’re actually losing money.

Also if you’re getting raises below the cost of living increase (which most people are), you’re losing money. If you get laid off, which hundreds of thousands of tech workers are, you’re definitely losing money. It’s not a great time right now.

Exactly. A 3% rise when inflation is 8% is effectively a paycut.

Have you tried skipping breakfast??? /s

Isn’t Denver an expensive city? Buying doesn’t mean instant low monthly payments. You gotta sit on that crap for ten years.

I dunno but my buddy just moved from his apartment in Brooklyn to Omaha and he was shocked the prices there were way too close to NYC prices for rent. He did go from a 1BD to 2BD but the cost difference per ft² was almost the same. Like $200 difference.

I’ve heard similar stories all across Canada as well, I think landlords have unchecked greed these days because people will end up paying no matter what they have to sacrifice you have a roof over their head.

Yeah, I always laugh at those median house prices because it’s impossible to find a house for that.