One in 4 middle-income new homeowners — twice as many as a decade before — are buying into cost-burdened situations.

The share of middle-class Americans who are buying wallet-squeezing homes has more than doubled in the previous 10 years.

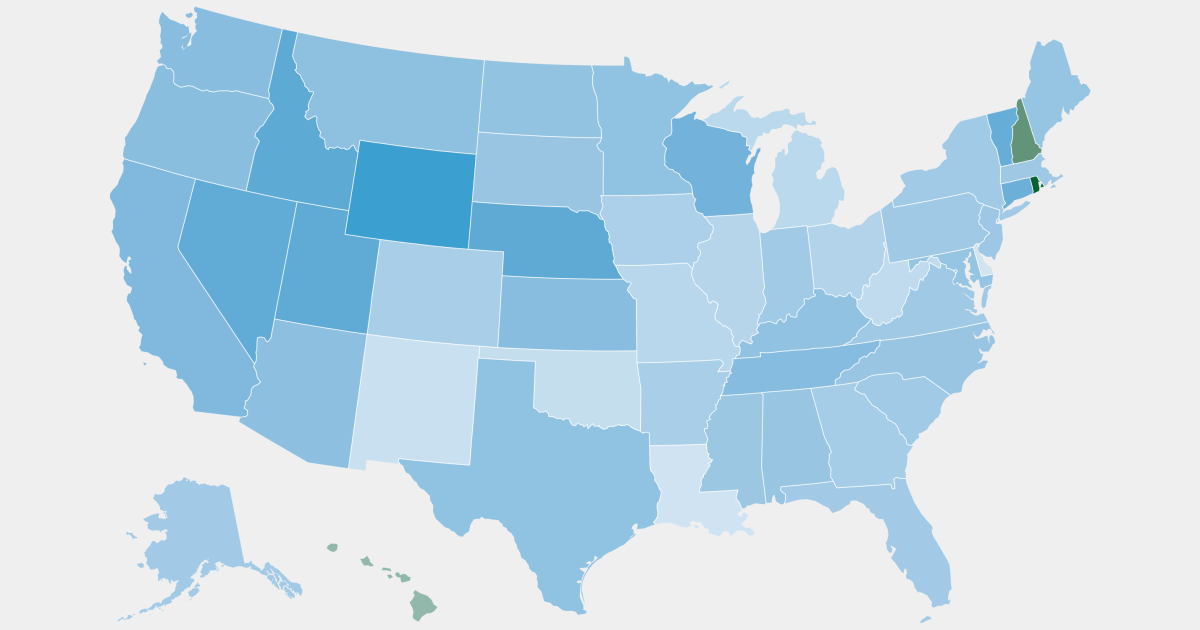

Almost 30% of middle-class homeowners bought homes with monthly payments costing more than 30% of their income in 2022, an NBC News analysis of Census Bureau data found. That’s more than twice the share from 2013, with experts warning it leaves many households with less money for groceries and emergencies and less able to get ahead in the future.

That “cost-burdened” benchmark — in which a household devotes over 30% of income to housing costs — is a widely used measure of affordability for both homeownership and renting. The Census Bureau measures housing costs against it, and the Department of Housing and Urban Development has used it for decades.

I have been house hunting for over a year. I don’t have crazy requirements…I want a 3 bedroom house with a sub basement (tornadoes) and a fenceable yard within an hour of work.

The average price for that around here is 425k. A house that needs major work might only go down to 300k.

Down payment on a 300k house is 60k. A 240k mortgage plus taxes and insurance is $2100/month. $2100 is 30% of $7000. That’s a $140k salary. The median income in my county is 78k.

I make above that, have 200k for a down payment, and am still struggling to find a place.

[Edit] fixed math

Might want to double check your math there. $2,100 is 30% of a gross $72,000 salary. That’s under your median income target.

You’re right, I estimated 40% to taxes/insurance/etc and jumped to typoed it to 240k (which I then changed to 200k+ because of the estimate)

But the point remains that making the median salary only affords you a house in terrible condition. If something is listed for anything less than 400k, it’s all but guaranteed that there’s major structural or mechanic work needing to be done…

And it’s not natural inflation - the houses listed for 450k today were 350-375k a year ago.

Down payment is not $60k. That’s only if you want to avoid PMI. That said, putting down less means several hundred more a month in payment.

Also, not sure how you are doing the math to get to a required $200k income. $7k/month is $84k/year. Even with taxes, that is a little over $100k.

deleted by creator

Maybe you are having a hard time finding a home because you are bad at math.

$7000/mo (even assuming take-home pay after insurance and 401k infusions, NOT gross salary) is more like $150k, not $200k. And that is in a high tax state like CA. $200k with 30% taxes is $140k, which is over $11k/month.